Many Australians approaching retirement believe they must have very limited savings to qualify for the Age Pension. However, the pension eligibility rules are often more flexible than people expect.

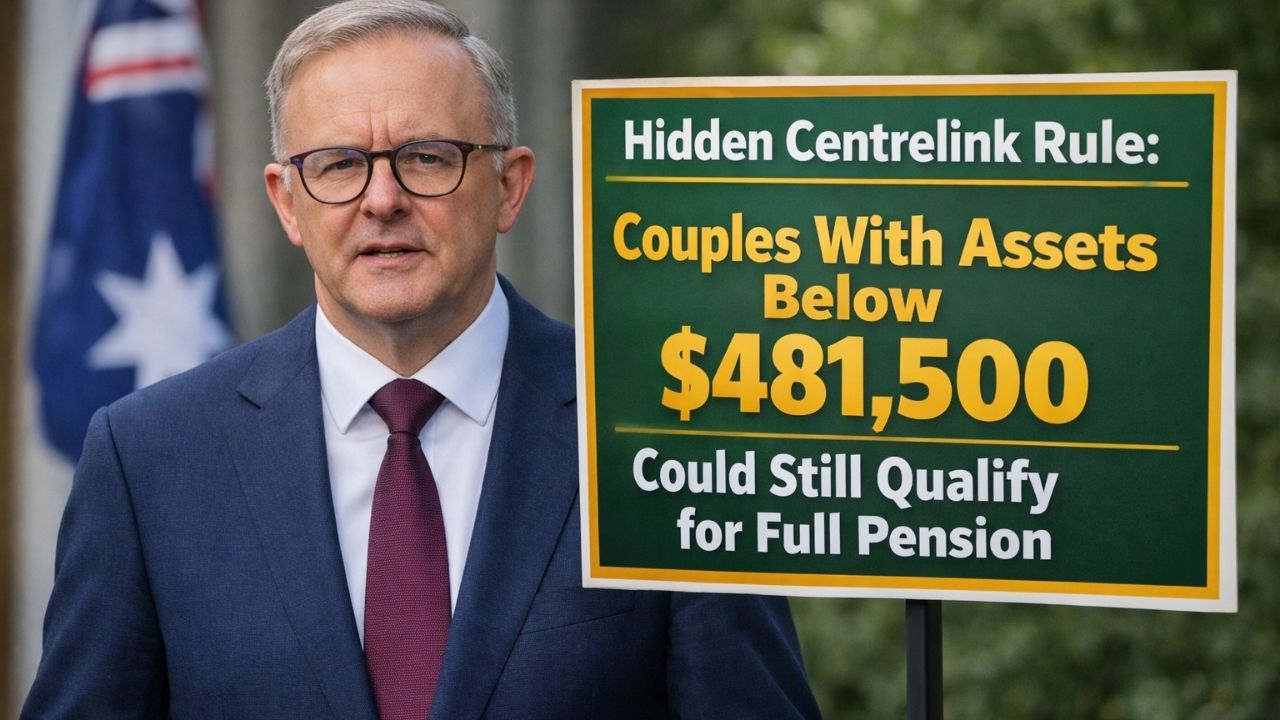

Under current guidelines, couples who own their home and have assets below approximately $481,500 may still qualify for the full Age Pension, provided they meet income and residency requirements.

Because these rules are not always widely understood, some retirees underestimate their potential eligibility for pension support.

How the Age Pension Asset Test Works

The asset test evaluates the total value of certain assets owned by pension applicants.

Assets that may be assessed include:

- Savings accounts

- Shares and investments

- Superannuation balances (in some cases)

- Investment properties

- Vehicles and valuables

However, the family home is generally excluded from the asset test.

Why the Asset Threshold Matters

The asset threshold determines whether applicants qualify for:

- The full Age Pension

- A partial pension

- No pension payment

Couples with assets below the threshold may receive the full payment if they also meet income requirements.

Real Stories Behind Pension Eligibility

Brisbane retiree Mark Collins says he was surprised to learn he still qualified for the pension.

“I thought my savings would make me ineligible,” he said.

Meanwhile, Sydney resident Mei Chen says understanding the asset test helped her plan retirement.

“Knowing the rules helps you make better financial decisions,” she explained.

These experiences show how pension rules can affect retirement planning.

Government Perspective on Pension Eligibility

Officials say the Age Pension is designed to support retirees who need financial assistance.

A Services Australia spokesperson explained that the system balances personal savings with government support.

“The asset and income tests ensure payments are directed toward those who need them most,” the spokesperson said.

Expert Insight: Planning Around Asset Thresholds

Financial planners say understanding pension rules can help retirees manage their savings more effectively.

Strategies may include:

- Reviewing investment structures

- Managing superannuation withdrawals

- Monitoring asset values

Careful planning can help retirees maximise retirement income.

Comparison of Asset Thresholds

| Household Type | Full Pension Asset Limit |

|---|---|

| Single Homeowner | Lower threshold |

| Couple Homeowners | Around $481,500 |

| Non-Homeowners | Higher threshold |

Exact thresholds may change during indexation reviews.

What Couples Should Know

Couples approaching retirement should review their financial situation and check how their assets affect pension eligibility.

Understanding both the income and asset tests can help retirees determine whether they qualify for full or partial pension payments.

Consulting financial advisers or reviewing Centrelink information can also help retirees make informed decisions.

Frequently Asked Questions

1. What is the Age Pension asset test?

A financial assessment used to determine pension eligibility.

2. Are homes counted as assets?

The primary residence is generally excluded.

3. What is the full pension asset limit for couples?

Around $481,500 for homeowners.

4. Can couples receive partial pensions?

Yes, if their assets exceed the full pension threshold.

5. Do investments count as assets?

Yes, shares, savings, and investment properties are assessed.

6. Do super balances count?

Certain superannuation balances may be included.

7. Why are asset tests used?

To ensure payments go to those who need them most.

8. Can asset limits change?

Yes, thresholds may be updated through indexation.

9. Should retirees review their assets regularly?

Yes, regular reviews help ensure accurate pension calculations.

10. Can retirees reduce assets to qualify?

Financial decisions should be made carefully and legally.

11. Where can couples check their eligibility?

Through Centrelink services or financial advisers.

12. Do income rules apply as well?

Yes, the income test also affects pension eligibility.

Leave a Comment